SA105 UK Property Income Tax Report User Guide

Quick Navigation

What is SA105?

SA105 is the UK property income supplement form required by HM Revenue and Customs (HMRC). It is filed as part of your Self Assessment Tax Return. If you own rental properties in the UK, you need to complete this form each year to report your rental income and related expenses.

RentPackage provides an SA105 report feature that automatically summarizes your rental income and expenses, making UK tax preparation simple and efficient.

How to Use

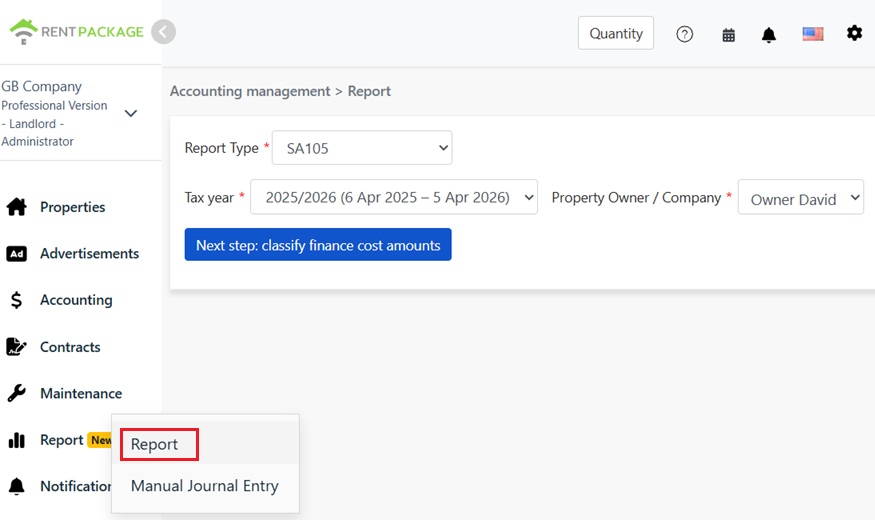

Step 1: Select Report Type and Tax Year

- Access the Report: Go to function list → Reports → Select "SA105" as the report type

- Select Tax Year: The dropdown will display complete tax year ranges, e.g., "2025/2026 (6 Apr 2025 - 5 Apr 2026)"

Step 2: Select Owner or Company

In the "Owner/Company" dropdown, select the entity for which you want to generate the report:

- Company: If you hold properties under a company name, select the corresponding company

- Owner: If you are a self-managing landlord or sublandlord, select the corresponding owner name

After selection, click "Next: Allocate Finance Costs".

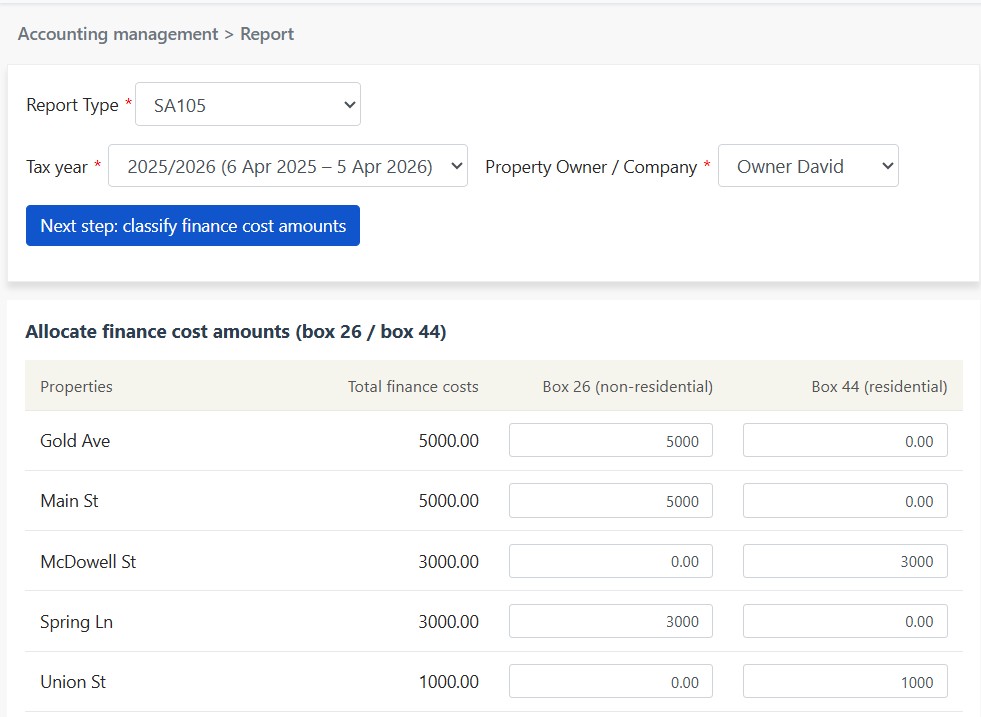

Step 3: Allocate Finance Costs (Box 26 / Box 44)

When you click "Allocate Finance Costs", the system retrieves the total amount from all accounts mapped to "Box 26/44 Finance Costs" and displays a screen for you to allocate the amount between Box 26 and Box 44:

| Property | Total Finance Costs | Box 26 (Non-Residential) | Box 44 (Residential) |

|---|---|---|---|

| 123 High Street | 0.00 |

Allocation Rules:

- Box 26 (Non-Residential): Fully deductible as an expense against rental income

- Box 44 (Residential): Not directly deductible; instead receives a 20% tax credit

- The system defaults all amounts to Box 44. For each property, Box 26 + Box 44 must equal the total finance costs

- For mixed-use properties (residential and commercial), allocate the amounts proportionally based on usage

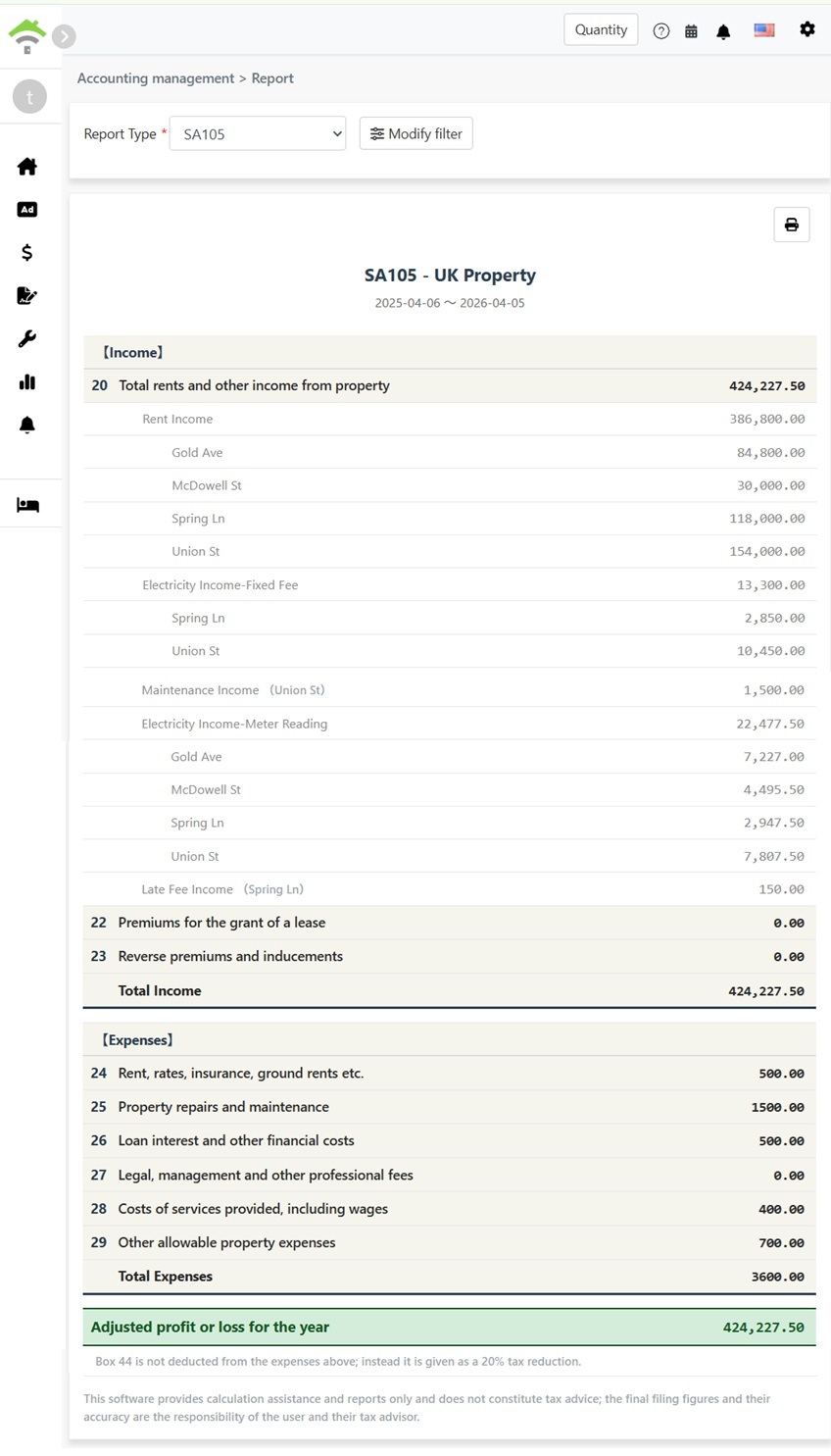

Step 4: Generate Report

- After confirming the finance cost allocation is correct, click "Generate Report"

- The system will generate an SA105 report showing:

- Income: Lines 20-23 - Rental income, lease premiums, etc.

- Expenses: Lines 24-29 - Allowable property expenses

- Adjusted Profit/Loss for the Year: Total Income - Total Expenses

- Residential Finance Costs: Line 44 - Residential mortgage interest (20% tax credit)

- You can print the report or export it as a PDF for your tax preparation records

Box 26 vs Box 44 Explained

| Item | Box 26 (Non-Residential) | Box 44 (Residential) |

|---|---|---|

| Property Type | Commercial properties, offices, shops, etc. | Residential lettings |

| Tax Treatment | Fully deductible as an expense | Not deductible; receives 20% tax credit instead |

| Report Location | Line 26: Loan interest and other financial costs | Line 44: Residential property finance costs |

Example:

Suppose you have a mixed-use property with total loan interest of £10,000, where 30% is for commercial use and 70% is for residential use:

- Box 26 (Non-Residential): £10,000 × 30% = £3,000 (fully deductible)

- Box 44 (Residential): £10,000 × 70% = £7,000 (20% tax credit = £1,400)

How to Set Up Chart of Accounts for SA105?

To map an account to finance costs:

- Go to Accounting → Chart of Accounts

- Find the account you want to map (e.g., Loan Interest)

- Set the SA105 Box to "Box 26/44 Finance Costs". The system will then automatically include this account's amounts in the finance costs total

To add finance cost transactions (two methods):

- Add to Lease Period: Add a transaction in the property's lease period using an account mapped to "Box 26/44 Finance Costs"

- Add Journal Entry: Create a journal entry using an account mapped to "Box 26/44 Finance Costs"

Amounts added through either method will be automatically included in the finance costs total.

Frequently Asked Questions

Does UK tax allow depreciation deductions?

No. Unlike the US Schedule E, UK property income tax does not have a depreciation field. In the UK, property depreciation is typically only relevant when calculating Capital Gains Tax upon sale of the property.

Why is my total finance cost showing as 0?

Please ensure your chart of accounts is correctly configured with SA105 Box set to "Box 26/44 Finance Costs". If not configured, the system will not include that account's amounts in the finance costs total.

Can Box 26 + Box 44 exceed the total finance costs?

No. The system validates that for each property, Box 26 + Box 44 must equal the total finance costs for that property.

Can I manually enter the total finance cost amount on the report page?

No. Unlike Schedule E depreciation, SA105 finance cost totals can only come from lease periods or journal entries. This design ensures accuracy and prevents discrepancies with your actual accounting records.

Why does the UK tax year run from 6 April to 5 April?

This is the official UK tax year as defined by HMRC. Unlike the standard calendar year (January to December), the UK tax year begins on 6 April each year and ends on 5 April of the following year.

SA105 Field Reference

【Income】

| Box | Field Name | Description |

|---|---|---|

| 20 | Total rents and other income from property | Total rental income and other property income |

| 22 | Premiums for the grant of a lease | Premiums received for granting a lease |

| 23 | Reverse premiums and inducements | Reverse premiums and inducements received |

【Expenses】

| Box | Field Name | Description |

|---|---|---|

| 24 | Rent, rates, insurance, ground rents etc. | Ground rent, rates, insurance premiums |

| 25 | Property repairs and maintenance | Repairs and maintenance costs |

| 26 | Loan interest and other financial costs | Finance costs for non-residential properties (fully deductible) |

| 27 | Legal, management and other professional fees | Legal fees, property management fees, accountant fees |

| 28 | Costs of services provided, including wages | Service costs including employee wages |

| 29 | Other allowable property expenses | Other allowable expenses not listed above |

【Residential Finance Costs】

| Box | Field Name | Description |

|---|---|---|

| 44 | Residential property finance costs | Finance costs for residential properties (20% tax credit) |